Second pillar buyouts: optimize your tax benefits

Second pillar buyouts: optimize your tax benefits

In the Swiss tax context, buy-ins in the 2nd pillar of professional pension savings represent a powerful lever to reduce one's tax burden while strengthening financial security in retirement.

This strategy is particularly relevant for self-employed individuals and employees wishing to optimize their wealth situation.

Why make a buy-in to the 2nd pillar?

Payments made into the 2nd pillar are deductible from taxable income, allowing for immediate tax savings.

The buy-in improves retirement benefits, in case of disability or death, while increasing the capital accessible upon retirement or early departure.

It is an attractive alternative compared to other investments, as assets in the 2nd pillar benefit from favorable taxation and are not taxed until withdrawal.

Who can benefit from it?

Individuals who have not contributed during certain years (studies, expatriation, change of professional status) or who have joined a new employer's plan can fill in the gaps of the missing years.

Self-employed individuals who have chosen to join a professional pension plan.

Any employee wishing to maximize their progression towards the legal maximum of the 2nd pillar capital.

Terms and limits of buy-ins

The redeemable amount is defined by the pension fund based on salary, contribution rate, and missing years of contribution.

It is possible to spread buy-ins over several years to optimize the tax advantage over time.

Attention: restrictions apply, especially in the case of early withdrawal for the purchase of a primary residence or if moving abroad.

Precautions and advice

Check with the pension fund the exact redeemable amount and simulate the tax impact before any operation.

Anticipate personal projects (primary residence, expatriation) as these influence the optimal strategy.

Be attentive to the rules regarding restitution in case of early withdrawal or change of marital status.

For tailored support, RidgeRock Partners offers a personalized analysis of your wealth situation, taking into account the buy-in opportunities of the 2nd pillar and the tax implications according to your canton of residence.

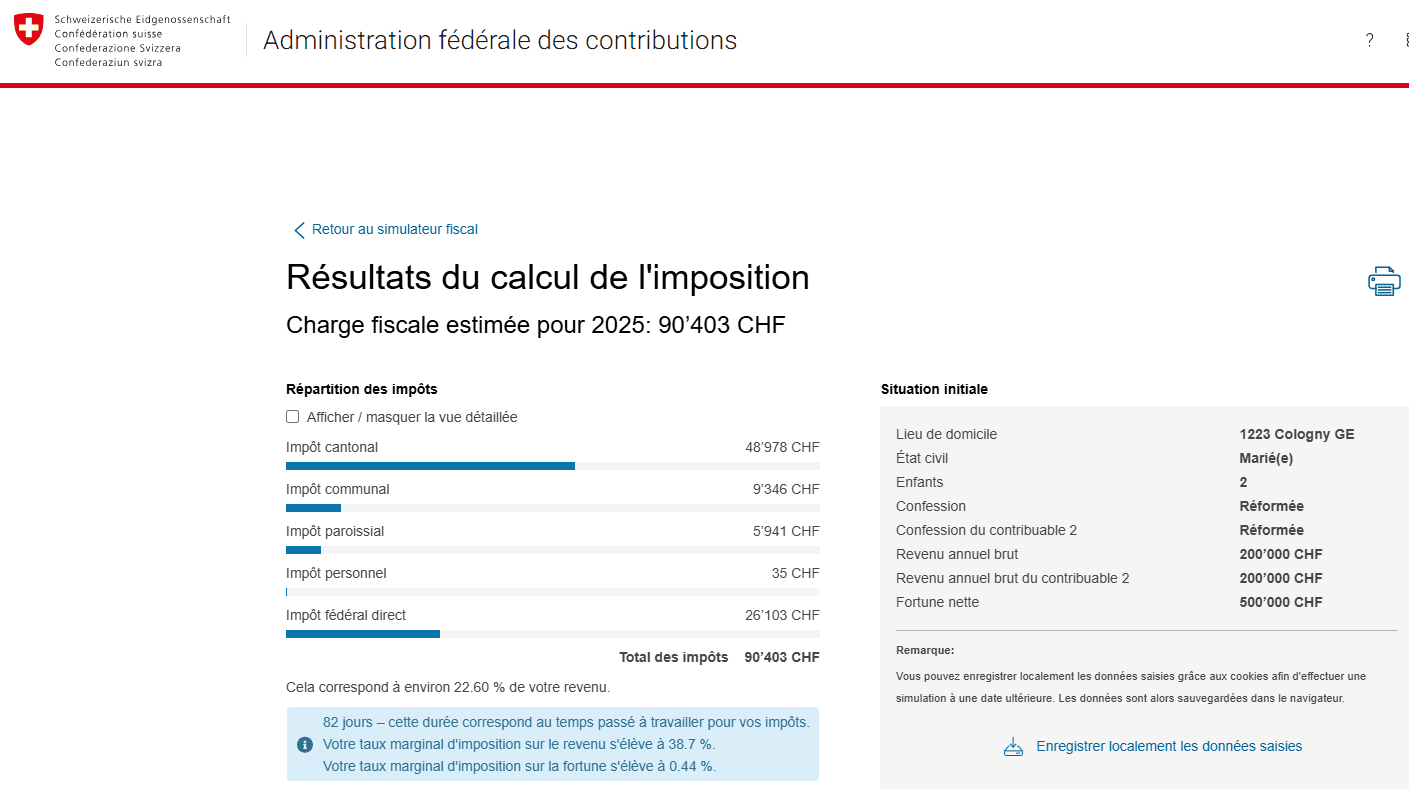

Practical example: Couple in Cologny

Let’s take the case of a married couple aged 50 with two children residing in Cologny, Geneva.

Their annual gross income amounts to CHF 400,000 and they are tenants. Their cumulative taxable income at the cantonal and federal level is CHF 313,466, with a marginal tax rate of 38.7%.

The couple decides to each make a buy-in of CHF 25,000 in their pension fund for the current year.

Total amount of buy-ins: CHF 50,000

Tax savings:

50,000×38.7%=19,350 CHF less in taxes!

This means that by investing CHF 50,000 in their professional pension, the couple benefits from an immediate reduction of their tax bill by nearly CHF 19,350, while improving their long-term financial security.

In the Swiss tax context, buy-ins in the 2nd pillar of professional pension savings represent a powerful lever to reduce one's tax burden while strengthening financial security in retirement.

This strategy is particularly relevant for self-employed individuals and employees wishing to optimize their wealth situation.

Why make a buy-in to the 2nd pillar?

Payments made into the 2nd pillar are deductible from taxable income, allowing for immediate tax savings.

The buy-in improves retirement benefits, in case of disability or death, while increasing the capital accessible upon retirement or early departure.

It is an attractive alternative compared to other investments, as assets in the 2nd pillar benefit from favorable taxation and are not taxed until withdrawal.

Who can benefit from it?

Individuals who have not contributed during certain years (studies, expatriation, change of professional status) or who have joined a new employer's plan can fill in the gaps of the missing years.

Self-employed individuals who have chosen to join a professional pension plan.

Any employee wishing to maximize their progression towards the legal maximum of the 2nd pillar capital.

Terms and limits of buy-ins

The redeemable amount is defined by the pension fund based on salary, contribution rate, and missing years of contribution.

It is possible to spread buy-ins over several years to optimize the tax advantage over time.

Attention: restrictions apply, especially in the case of early withdrawal for the purchase of a primary residence or if moving abroad.

Precautions and advice

Check with the pension fund the exact redeemable amount and simulate the tax impact before any operation.

Anticipate personal projects (primary residence, expatriation) as these influence the optimal strategy.

Be attentive to the rules regarding restitution in case of early withdrawal or change of marital status.

For tailored support, RidgeRock Partners offers a personalized analysis of your wealth situation, taking into account the buy-in opportunities of the 2nd pillar and the tax implications according to your canton of residence.

Practical example: Couple in Cologny

Let’s take the case of a married couple aged 50 with two children residing in Cologny, Geneva.

Their annual gross income amounts to CHF 400,000 and they are tenants. Their cumulative taxable income at the cantonal and federal level is CHF 313,466, with a marginal tax rate of 38.7%.

The couple decides to each make a buy-in of CHF 25,000 in their pension fund for the current year.

Total amount of buy-ins: CHF 50,000

Tax savings:

50,000×38.7%=19,350 CHF less in taxes!

This means that by investing CHF 50,000 in their professional pension, the couple benefits from an immediate reduction of their tax bill by nearly CHF 19,350, while improving their long-term financial security.

Need an outside perspective on your situation?

Our team answers your questions for free.

Need an outside perspective on your situation?

Our team answers your questions for free.

International Center Cointrin

Route de Pré-Bois 20, CP 228,

1215 Geneva, Switzerland

Our Expertise

© 2025 RidgeRock Partners. All rights reserved.

© 2025 RidgeRock Partners. All rights reserved.

International Center Cointrin

Route de Pré-Bois 20, CP 228,

1215 Geneva, Switzerland

Our Expertise

© 2025 RidgeRock Partners. All rights reserved.