For many cross-border workers, the Swiss 2nd pillar is often seen as a simple retirement tool. In reality, it can also become a very interesting tax-optimization lever, but only within a specific framework.

The key point to remember is simple: the deduction in France of 2nd pillar buybacks concerns cross-border workers whose salary is taxed in France, that is, mainly those who work in the 8 cantons covered by the cross-border agreement. In Geneva, where tax is withheld at source in Switzerland, the logic is different and the issue does not arise in the same terms.

Why this topic interests cross-border workers so much

Buying back into the 2nd pillar consists of voluntarily paying an additional amount into your Swiss pension fund in order to fill a pension gap and improve your future benefits.

This approach can have a double benefit: preparing for retirement more comfortably and, in some cases, reducing the tax bill for the year of payment.

This is precisely what raises many questions among French residents working in Switzerland. Between the Franco-Swiss tax treaty, differences between cantons, and the rules specific to French retirement, it is easy to confuse relevant optimization with a false good idea.

The key rule: everything depends on the canton where you work

From a tax perspective, not all cross-border workers are treated equally. The 1983 cross-border tax agreement provides that employees residing in France and working in 8 Swiss cantons are taxed in France on their salaries.

The cantons concerned are as follows:

Bern

Solothurn

Basel-Stadt

Basel-Landschaft

Vaud

Valais

Neuchâtel

Jura

In these cantons, the Swiss salary is declared in France and taxed according to French rules. It is within this framework that 2nd pillar buybacks can produce a concrete French tax effect.

Geneva: a special regime

Geneva operates under a different mechanism. For cross-border workers who work there, tax is in principle withheld directly at source in Switzerland by the employer, according to Geneva tax scales.

This completely changes the analysis. The issue is then no longer to know what amount of buyback can be deducted from taxable income in France, but rather what effect the buyback has on Swiss taxation and on the overall wealth-planning strategy.

In other words, when a client works in Geneva, you should not reason with the French CNAV 12-quarter scale as if they were taxed in France on their salary. This rule is primarily relevant for cross-border workers in the 8 cantons covered by the specific agreement.

What the French tax authorities say

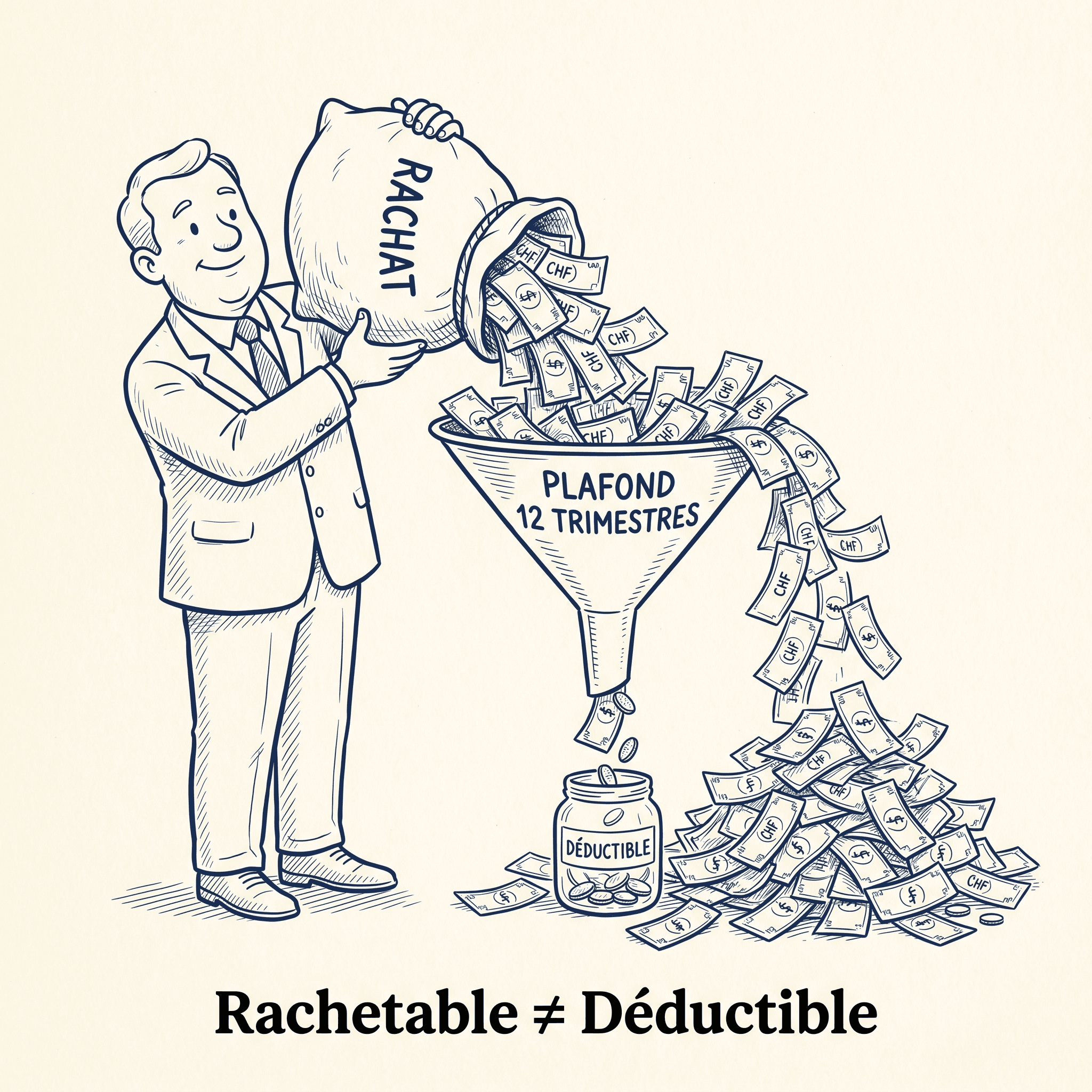

A written response from the French tax administration dated April 23, 2026, issued regarding a French resident employed in the canton of Vaud, provides very useful clarification. It confirms that LPP "2a" contribution buybacks may be deductible in France, but only up to the limit of 12 quarters assessed according to the CNAV scale.

This clarification is important because it avoids a common mistake: thinking that any buyback made in Switzerland is automatically deductible in France. In reality, France allows the deduction, but within a limit that corresponds to the theoretical cost of buying back French retirement quarters.

The administration also points out that the Swiss 3rd pillar is not deductible in France. It is therefore important to distinguish between payments made into the LPP 2nd pillar and those made into optional individual retirement wrappers.

How the 12-quarter limit works

French rules do not simply take the actual amount paid into the pension fund. They compare that payment with a theoretical cap calculated from the CNAV scale, that is, the scale used in France for certain retirement-quarter buybacks.

In practice, the cap depends in particular on:

the taxpayer's age;

their income level;

the cost of one quarter under the CNAV scale;

the overall limit of 12 quarters.

The principle is therefore as follows:

determine the cost of one quarter under the CNAV scale;

multiply that cost by 12;

compare that cap with the buyback actually paid in Switzerland.

If the payment is below the cap, it can in principle be fully deductible. If it exceeds it, only the portion remaining within the limit of 12 quarters is deductible in France.

Concrete example: age 40 and CHF 100,000 in annual gross salary

Let's take a simple, clear case. A French tax resident, aged 40, works in the canton of Vaud and earns an annual Swiss gross salary of CHF 100,000. Because Vaud is part of the 8 cantons covered by the cross-border agreement, his salary is taxed in France.

Suppose his pension fund allows him to make a buyback of CHF 35,000. Many taxpayers think such a payment will automatically be deductible in full. That is not always correct.

The right method is to first calculate the CNAV cap corresponding to his age and reference income. If, for illustration, the theoretical value of 12 quarters comes to CHF 48,000, then a CHF 35,000 buyback could be fully deductible. If the client paid CHF 60,000, only the portion within the CHF 48,000 limit would be tax-recognized in France.

This example shows one essential thing: the CHF 100,000 salary is not, by itself, the deduction cap. It mainly serves to place the taxpayer in the right bracket of the scale, while the true tax limit remains the 12-quarter CNAV cap.

The most common mistake

The most common mistake is to reason only from the Swiss pension fund certificate. Yet the buyback capacity authorized by the fund and the amount deductible for tax purposes in France are two different notions.

A client may very well have the right to buy back CHF 80,000 or CHF 100,000 into their Swiss pension fund, while only a fraction of that amount is actually deductible on their French return. That is precisely why a wealth-planning decision must be made before the payment, not after.

What good wealth advice should take into account

For an affected cross-border worker, a 2nd pillar buyback should never be considered in isolation. You need to cross-check the buyback capacity given by the Swiss fund, the French deduction limit, the retirement horizon, the family situation, available liquidity, and the other retirement wrappers already used.

A serious analysis therefore needs to answer four simple questions:

does the client work in one of the 8 cantons where salary is taxed in France?

is it really a buyback into the 2nd pillar and not a payment into the 3rd pillar?

what is the real deduction cap in light of the CNAV scale?

does the buyback remain worthwhile beyond its immediate tax benefit?

What to remember

Buying back into the 2nd pillar can be an excellent tool for a cross-border worker residing in France, provided it is done within the right tax framework. The French deduction primarily targets employees in the 8 cantons covered by the cross-border agreement, whose income is taxed in France.

For Geneva, the logic is different because tax is withheld at source in Switzerland. In that case, the focus is first on Swiss taxation, not on the French limit of 12 CNAV quarters.

Before any significant buyback, it is therefore essential to verify not only the amount that can be bought back through the pension fund, but above all the amount actually deductible in France. It is this difference that turns an ordinary retirement-saving operation into a well-managed wealth strategy.